Understanding Your First Invoice: What It Is & Why It Matters (Plus FAQs)

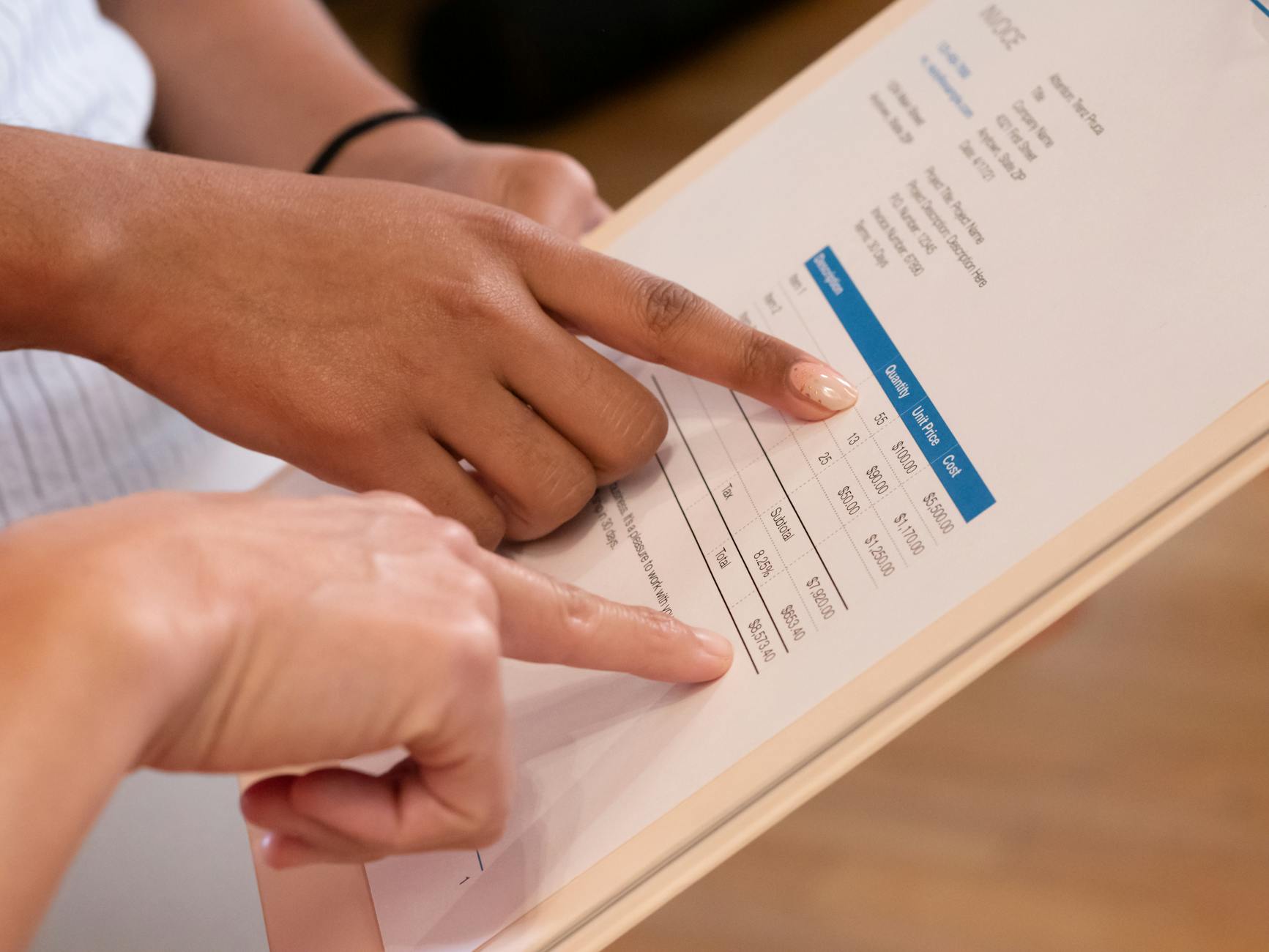

Your first invoice isn't just a piece of paper; it's a critical document marking the official start of a financial relationship with a vendor or service provider. At its core, an invoice is a detailed request for payment, outlining the goods or services provided, their quantities, unit prices, and the total amount due. Beyond the immediate payment request, this initial invoice serves several vital functions. It acts as a legal record of the transaction, providing proof of purchase for your own accounting and potential tax purposes. Furthermore, it often establishes the payment terms and conditions, such as the due date and any late payment penalties, setting the precedent for future interactions. Understanding every line item, from service descriptions to applicable taxes, is paramount to ensuring accuracy and avoiding disputes down the line.

Failing to properly understand and process your first invoice can lead to a cascade of negative consequences, impacting both your immediate finances and long-term business relationships. Ignorance of payment deadlines can result in late fees, damaging your credit with the vendor and potentially leading to service interruptions. Moreover, an unexamined invoice might contain errors, such as incorrect billing for services not rendered or miscalculated totals, which can cost your business money if not caught promptly. It's not just about paying; it's about verifying. This initial document also provides an excellent opportunity to review the agreed-upon scope of work against what was actually delivered and billed.

Treat your first invoice as more than a bill; consider it a foundational document for a transparent and healthy financial partnership.

To issue an invoice, start by gathering all necessary details such as your business information, client details, a unique invoice number, date, and a clear breakdown of products or services provided. Ensure each item includes a description, quantity, unit price, and total, then calculate the grand total including any applicable taxes or discounts. For more detailed guidance on how to issue an invoice, consider using accounting software or templates to streamline the process and maintain accuracy.

Crafting Your Invoice: Essential Elements & Practical Tips for Success

An invoice isn't just a request for payment; it's a critical component of your business's financial health and professional image. To ensure smooth transactions and avoid misunderstandings, every invoice you issue should clearly detail essential information. This includes your business's legal name and contact information, along with the client's corresponding details. Crucially, each invoice needs a unique identification number (for easy tracking), the date of issuance, and a payment due date. Furthermore, a comprehensive breakdown of services or products provided is paramount. This should encompass a clear description, quantity, unit price, and the total amount for each item. Don't forget to specify any applicable taxes or discounts, culminating in the grand total due. A well-structured invoice, therefore, acts as a transparent record for both parties, fostering trust and accountability.

Beyond these fundamental elements, several practical tips can elevate your invoicing process from merely functional to truly successful. Firstly, consider incorporating your brand's logo and color scheme to maintain a consistent professional appearance. This reinforces your brand identity and makes your invoices instantly recognizable. Secondly, clearly state your preferred payment methods (e.g., bank transfer, credit card, PayPal) and provide all necessary details for each. Additionally, including your payment terms – such as

"Payment due within 30 days of invoice date"– helps set clear expectations. For recurring clients, discuss the possibility of automated invoicing to streamline the process for both sides. Finally, always maintain meticulous records of all invoices sent and payments received. This disciplined approach not only simplifies tax preparation but also provides a robust audit trail, safeguarding your financial operations.